Life insurance, far beyond being a monthly commitment, emerges as a strategic tool for wealth accumulation and legacy planning. This not only assures financial security for loved ones following your demise but also functions as an investment pathway. As we delve deeper, the spotlight falls on max-funded life insurance – a potent addition to your retirement portfolio, offering a dual advantage of growth and security.

Max-funded life insurance encapsulates more than just a safety net; it’s an opportunity to build a meaningful financial legacy. By infusing it into your retirement planning, you are setting the stage for potential wealth growth, while ensuring that your family’s future remains financially stable. Let’s explore and unravel the benefits of this remarkable financial instrument.

In this article, we are going to discuss the reasons why you should consider adding a max-funded life insurance policy to your retirement portfolio.

Table of Contents

What Is Overfunded Life Insurance?

Overfunded Life Insurance (OLI), often known as a Life Insurance Retirement Plan (LIRP), is an enticing prospect for those aiming to amass considerable savings while enjoying tax privileges. Designed for maximum early high cash value accumulation, these policies provide a blend of asset protection and tax benefits, making OLI an astute wealth-building strategy.

The Basics of Minimum Overfunding in Life insurance

The Power of Liquidity

Max-funded life insurance policies grant immediate access to your funds, unlike traditional retirement plans. This offers a level of liquidity that can be a game-changer in times of unforeseen expenses or investment opportunities.

Tax Efficiency

Overfunded life insurance policies stand out for their tax benefits. The cash value growth within the policy is tax-deferred, and in most cases, policy loans are tax-free. This makes max-funded life insurance a smart choice for tax-efficient wealth accumulation.

Protection Amid Volatility

In today’s volatile market landscape, max-funded life insurance offers a safeguard. The cash value in these policies is not subject to market risks, thereby providing a secure shield for your retirement corpus.

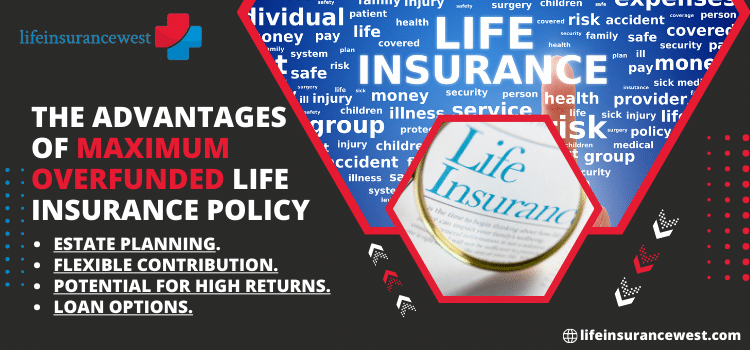

The Advantages of Maximum Overfunded Life Insurance Policy

- Estate Planning: Max-funded life insurance policies can also serve as an effective estate planning tool. The death benefit from the policy is generally tax-free and can be a significant financial support to your heirs.

- Flexible Contribution: Unlike many retirement plans, max-funded life insurance policies offer flexible contribution amounts. Policyholders can adjust the amount they contribute, which can be particularly beneficial during periods of financial uncertainty.

- Potential for High Returns: Max-funded life insurance policies have the potential for higher returns compared to traditional insurance policies. This is because a significant portion of the premiums is invested, potentially leading to higher growth rates.

- Loan Options: Policyholders have the opportunity to take out loans against their policy. These loans are typically tax-free and won’t affect the policy’s death benefit, provided the policy is not surrendered.

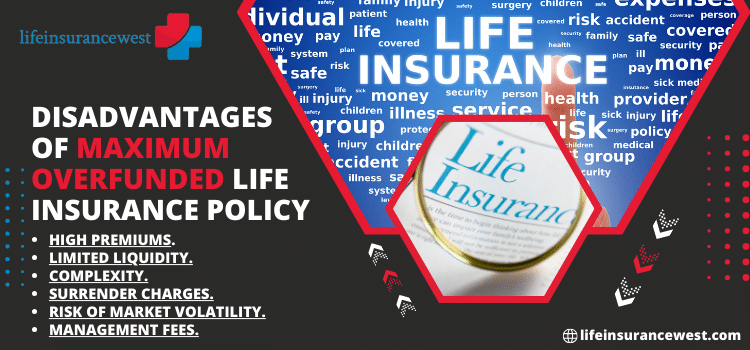

Disadvantages of Maximum Overfunded Life Insurance Policy

High Premiums:

One potential disadvantage of max-funded life insurance policies can be the high premiums. These are typically more expensive than traditional term life insurance policies due to the investment component.

Limited Liquidity:

In the early years of the policy, cash value may be limited due to costs associated with setting up the policy. This can limit your ability to take loans or make withdrawals from the policy.

Complexity: Max-funded life insurance policy

Max-funded life insurance policies can be complex for some individuals to understand. They combine the aspects of life insurance and investment, which requires a certain level of financial literacy to manage effectively.

Surrender Charges:

Early termination of the policy can attract surrender charges. These can significantly reduce the cash value, especially if the policy is surrendered in the first few years of its term.

Risk of Market Volatility:

Like any investment, max-funded life insurance policies are subject to the volatility of the market. While they have the potential for high returns, there’s also a risk of losing value if the investments perform poorly.

Management Fees:

Most max-funded life insurance policies come with management fees that can eat into the overall returns. These fees are for the management of the investment portion of the policy and can vary widely between insurance companies.

Reputation and Stability of the Insurance Company:

The performance and benefits of a max-funded life insurance policy can significantly depend on the reliability and stability of the insurance company. Policyholders need to conduct thorough research and consider the company’s reputation, financial stability, and customer service before purchasing a policy.

Now let’s look at a Maximum Over-funded policy design

A Maximum Over-funded policy design often entails higher premium payments which are used to increase the cash value. This overfunding approach, while it demands a larger investment, can potentially yield a more substantial cash value over time. However, it’s crucial for policyholders to understand that this design, like any other financial strategy, carries its own set of risks and benefits.

Choosing Between Minimum and Maximum Overfunded Life Insurance

Choosing Between Minimum and Maximum Overfunded Life Insurance

At the crossroads of minimum and maximum overfunded life insurance, your choice depends on personal financial factors. Consider your long-term financial goals, the level of risk you’re comfortable with, and your current economic capabilities.

Now, if you’re comfortable taking on more risk for the potential of higher returns, a maximum overfunded policy may be a suitable choice. This policy design requires higher premium payments. However, it offers the potential for a larger cash value accumulation over time. It’s a viable option if you can absorb the higher premiums and are comfortable with the inherent market risks.

On the other hand, a minimum overfunded life insurance policy may be more suitable for those looking for a more conservative approach. This policy design requires a lower outlay and holds lower risk. Yet, it still provides some potential for cash value growth, albeit at a slower rate. It’s an ideal choice for those who prefer stability and predictability in their investments.

Remember, both types of policies have their unique benefits and risks. It’s crucial to consult with a trusted financial advisor to understand these fully. Ultimately, your choice should align with your financial goals, risk tolerance, and economic capacity.

Best Options When to Choose Minimum And Maximum

- Maximum overfunded life insurance suits risk-takers.

- It requires higher premiums.

- Offers potential for larger cash value accumulation.

- Suitable for those with higher economic capacity.

- Minimum overfunded policies are conservative.

- These require a lower outlay.

- Offers cash value growth, albeit slower.

- Ideal for those preferring stability in investments.

- Understanding the risks and benefits is crucial.

- Consult a financial advisor before choosing.

- Ensure alignment with your financial goals and risk tolerance.

Common Uses for Max-Funded Indexed Universal Life

Max-Funded Indexed Universal Life

Max-funded Indexed Universal Life (IUL) insurance is a versatile financial tool.

Wealth Accumulation

Max-funded IUL enables efficient wealth accumulation. It provides an investment platform with considerable growth potential.

Income Generation

Through policy loans, Max-funded IUL can serve as a tax-efficient income stream during retirement.

Estate Planning

Max-funded IUL ensures a tax-free death benefit, offering a valuable tool for estate planning.

Using Minimum Overfunded Life Insurance

Minimum Overfunded Life Insurance

Stability and Affordability

Preferred by those seeking affordable, steady growth.

Lower Premiums

Requires less financial outlay compared to maximum overfunding.

Slower Cash Value Growth

Offers steady, albeit slower, wealth accumulation.

Risk Management

Ideal for investors valuing predictability and minimal risk.

Financial Advisory

Always consult an advisor before finalizing a choice.

How Much Does a Max-Funded IUL Insurance Policy Cost?

The cost of a Max-Funded IUL insurance policy can vary greatly. This is due to multiple factors. It is contingent upon the policyholder’s age, health status, and policy size, among others. Moreover, the amount of premium overfunding also plays a significant role. To illustrate, a younger, healthier individual might pay lesser premiums.

On the other hand, an older individual with health issues may have higher premiums. It’s alsoworth notinge that a larger policy size generally commands a higher premium. The same applies to policies with higher overfunding. Therefore, prospective policyholders should conduct a thorough evaluation. When doing so, consider all these factors.

Additionally, they should seek guidance from financial advisors. This is to ensure that their choice aligns with their financial objectives. It is also to ensure it suits their risk tolerance profile. Lastly, obtaining multiple quotes from various insurers is also a smart move. This allows for comparison and finding the most cost-effective policy.

What will a properly structured, maximum-funded Indexed Universal Life policy cost you?

Estimating the cost of a max-funded IUL policy is complex. Several factors influence this cost. Age, health, and policy size are key determinants. Premium overfunding level also impacts the cost. Younger, healthier individuals often pay lesser premiums. Conversely, older, less healthy individuals pay more. Large policies also command higher premiums. Remember to consult a financial advisor. Their expert advice aligns with your financial goals. Lastly, obtain quotes from various insurers. This helps you find the most economical policy.

Comparing Max-Funded IUL Insurances Policies to Other Financial Vehicles

The financial landscape is vast and diverse. Where does Max-Funded IUL stand? Let’s delve into this fascinating comparison.

First, we look at traditional savings accounts. These are safe, but yield low returns. In contrast, Max-Funded IUL offers potential for high returns. Yet, it comes with a risk – the market’s unpredictability.

Next, we compare with bonds. Bonds are stable and provide fixed income. However, their returns can’t match Max-Funded IUL’s potential.

Now, let’s consider mutual funds. They boast substantial gains, but also significant losses. On the other hand, Max-Funded IUL’s cash value is never negative.

Finally, we peek at 401(k)s. They’re great for employer-matching contributions. However, they lack the flexibility Max-Funded IUL policies offer.

In closing, every financial vehicle has its merits. Assessing them against Max-Funded IUL helps you choose wisely.

Conclusion

Navigating the financial terrain requires informed decisions. Max-funded IUL, with potential gains and flexibility, shines brightly. Yet, risks persist. Understand your financial requirements. Balance them with available options. Seek expert advice if needed. Ultimately, your financial journey is unique. Choose wisely, invest intelligently, and secure your financial future.

MaxLife+ Policy offers the perfect balance between risk and reward. Its benefits are unparalleled in the insurance industry, with cash value accumulation, death benefit protection, and policy loan options for a lifetime of security. With so many potential benefits, MaxLife+ is one of the best investments you can make. Explore your options today to find out how MaxLife+ can work foryou.

5 Common Life Insurance Myths?

Life insurance is too expensive.

I’m too young to buy life insurance.

Term life is better than whole life.

My employer-sponsored plan covers me enough.

My spouse’s policy will cover my family if something happens to me.

What Is a Contingent Beneficiary?

A contingent beneficiary is the next in line after the primary beneficiary. In case the primary cannot receive the benefits, they step in. It’s crucial to have both primary and contingent beneficiaries. Ensuring your benefits reach the right hands in any eventuality is crucial. This provides a safety net for your loved ones. Always review your beneficiaries to match current relationships. Please reach out to a financial advisor for more guidance. It’s your financial future, so make the right choices.

Is Cash Value Life Insurance Taxable?

It depends on the type of policy and how it was used. Generally, if you take out a loan against your cash value policy, then the amount borrowed is taxable when received as income. It’s also important to note that when you surrender a life insurance policy for its cash value, any earnings accumulated over the years are subject to taxation. Be sure to consult with a financial advisor to ensure you’re making the most of your policy and following IRS regulations.

What Benefits Does MaxLife+ Offer?

MaxLife+ offers a variety of benefits to meet your needs. These include:

Death Benefit Protection: MaxLife+ provides death benefit protection for your loved ones, ensuring both security and peace of mind.

Can I Change My Beneficiaries?

Yes, you can change your beneficiaries at any time. It’s recommended to review your beneficiaries annually or after significant life events such as marriage, divorce, the birth of a child, or the death of a beneficiary. To change your beneficiaries, contact your life insurance provider or financial advisor who can guide you through the process. drawbacks. The